Clients do not leave your brokerage because of price. They leave because your CSRs never called them back. They are not ignoring the book on purpose. They are drowning in suspense, re-keying the same client data into a different carrier portal for the fifth time today, and fielding back-to-back phone calls from irate clients hit with 20% rate hikes. The urgent eats the important. Proactive remarketing, pre-renewal reviews, cross-sell conversations, the "hero work" that actually retains accounts, never happens. And the retention ratio slowly bleeds.

Everyone in the industry knows the phrase "carrier portal fatigue." It describes the daily reality of managing dozens of distinct logins, each to a poorly designed proprietary website, just to retrieve a loss run, issue a COI, or process a routine endorsement. The AMS is supposed to be the single source of truth, but the moment a CSR has to bind a policy or check a claim status, they abandon it for the carrier's environment. The data fragmentation guarantees that the AMS is perpetually outdated, and leadership makes decisions on numbers that are wrong. For the full industry breakdown, see our insurance brokerages page.

The brokerages that scale in this market are the ones that free their CSRs from the busy work. Not with another login. Not with another SaaS platform your team has to learn. With invisible infrastructure that runs inside the tools your team already uses. This post walks through the seven highest-impact workflows to automate in an independent brokerage, what each one replaces, and the measurable outcomes that follow.

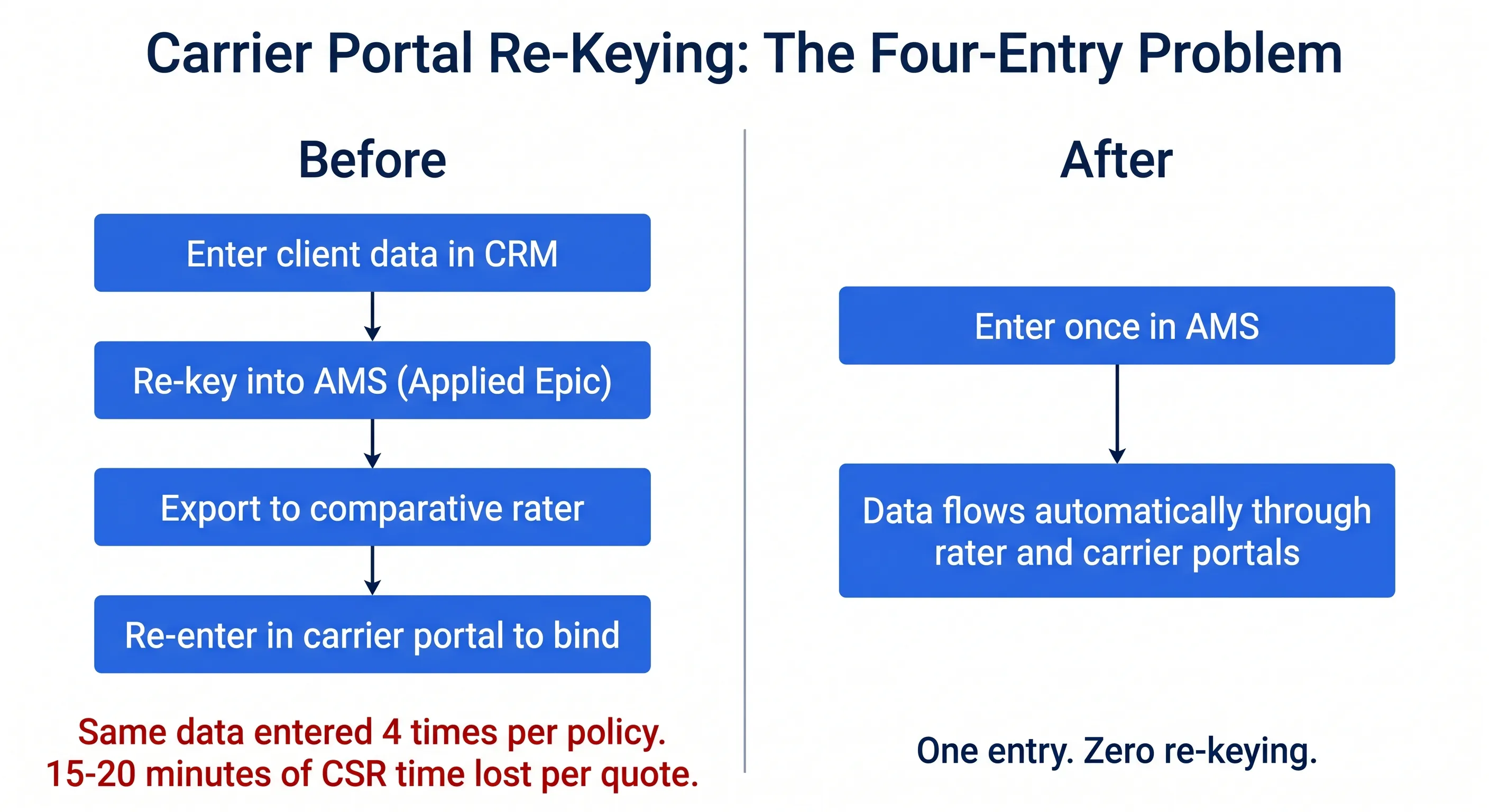

1. Carrier portal data re-keying.

The re-keying cycle is the single largest drain on brokerage profitability. A producer gathers client data on a discovery call and enters it into a CRM like AgencyZoom or Salesforce. They then re-key it into the AMS to create a client shell. They export the shell to a comparative rater like TurboRater or PL Rating. After running the rater and picking a winning quote, they log into the carrier's proprietary portal and re-key the exact same vehicle, property, and driver data a fourth time to bind the policy. Four systems, one data set, re-entered by hand each time.

The damage compounds. Carriers constantly update their underwriting questions, shift class codes, and tweak their rating algorithms. The AMS cannot keep pace, so "integrations" break or return stale quotes. Your CSR abandons the AMS entirely and works directly in the carrier environment, which means the AMS is perpetually out of date. A simple VIN update for a client takes 30 minutes of system-switching for what should be 10 seconds of actual decision-making.

What automation looks like: a single source of truth. Client data flows from the CRM into the AMS into the rater into the carrier portal automatically. No re-typing VINs. No copy-pasting property specs. Endorsements kick off in the AMS and the carrier portal updates itself in the background. Automation runs inside the tools you already use, so your CSRs do not learn a new system. They just stop re-keying. Recapture: 8 to 12 hours per CSR per week, redirected to the calls your clients actually need.

2. Renewal marketing and remarketing.

Here is how renewals fail today. A client's premium jumps 25% at renewal because of hard market conditions. They call your CSR, furious. The CSR spends 45 minutes de-escalating the call and defending the agency. They intend to remarket the policy to find a cheaper carrier, but they are back-to-back on similar calls for the rest of the day. By the time they can pull the expiring policy data and log into five carrier portals to run new quotes, the client has already called a competitor. The retention ratio bleeds one account at a time. Clients leave not because of the rate hike. They leave because you never called back.

What automation looks like: automatic remarketing the moment a rate increase crosses a threshold. The system flags every policy with a proposed renewal premium 15% or higher, pulls the policy data, and runs it through the comparative rater against every appointed carrier. Your CSR walks in Monday morning to a prioritized call list: clients most at risk of churning, each with three alternative quotes already run, ready to pick up the phone and save the account before the client has a reason to shop. Proactive retention becomes the default workflow instead of the thing that never happens.

3. Certificate of Insurance (COI) issuance.

Your commercial clients cannot step onto a job site or receive payment from a General Contractor without a valid COI proving specific liability and workers' comp coverages. They call the brokerage from the actual job site demanding one. The CSR stops whatever they were doing, opens the AMS, verifies coverage is active, generates an ACORD 25, and often has to obtain formal underwriter approval when the GC demands specific Additional Insured language or waiver of subrogation clauses. Each one takes 15 to 30 minutes. At renewal, a single commercial client with 100 certificate holders turns into a full-day manual reissue project.

What automation looks like: template-driven COI generation with automatic distribution. Clients can request a COI through a simple email or portal, the system verifies coverage status in the AMS, pulls the holder requirements from the contract, generates the ACORD 25 with the correct Additional Insured and waiver language, routes for underwriter approval only when required, and emails the completed certificate to the holder. Issuance drops from 20 minutes to under 1 minute. Your CSR handles exceptions, not the 95% of COIs that follow standard templates.

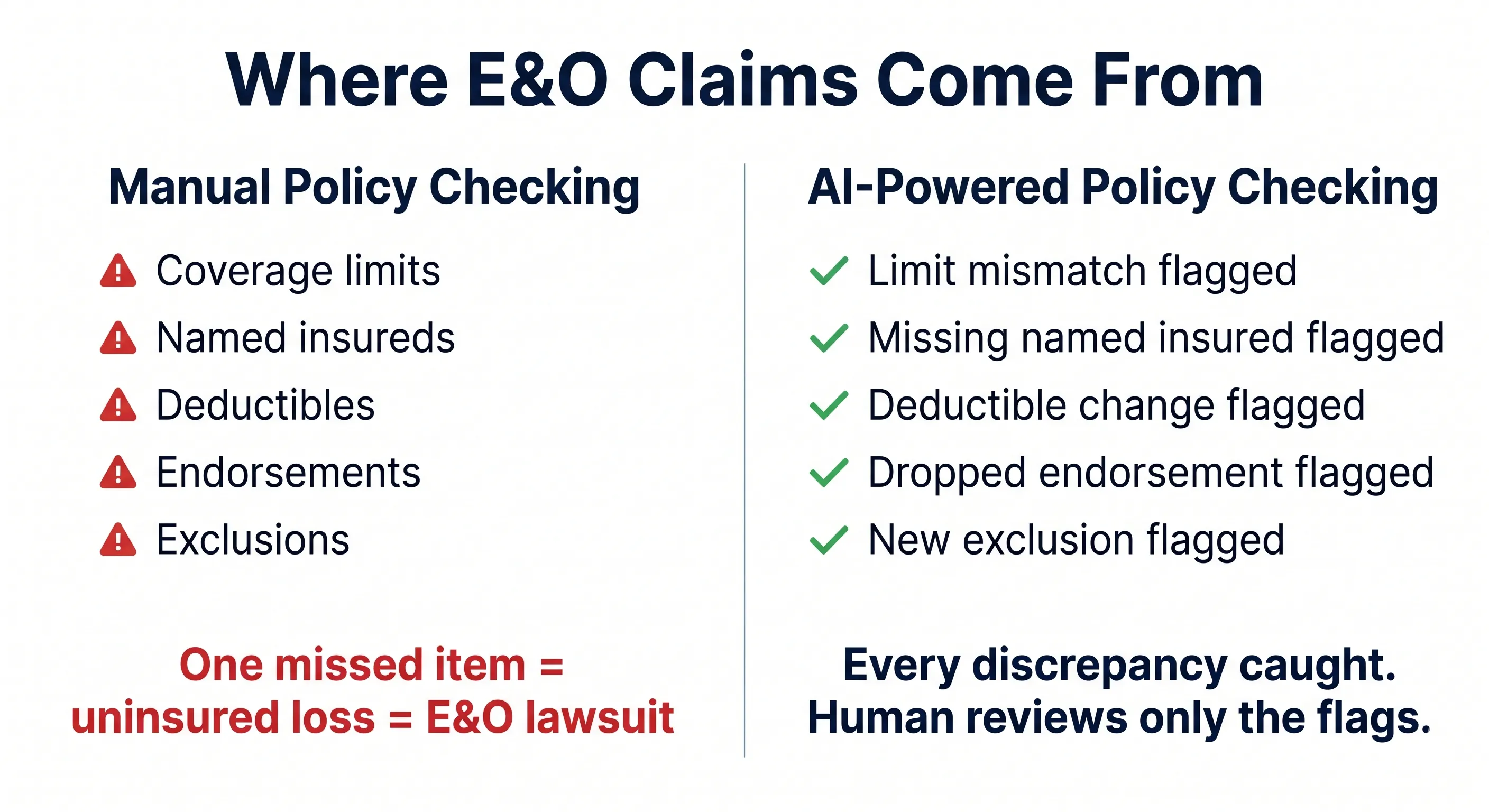

4. Policy checking against applications.

Policy checking is the workflow that keeps agency principals awake at night. A CSR has to compare a newly issued commercial policy (often several hundred pages) against the original quote, the binding instructions, and the expiring policy. They are looking for subtle discrepancies: a coverage limit that does not match, a deductible that shifted, a named insured that was misspelled, an endorsement that was supposed to be included but was not. A thorough manual check takes 2 to 4 hours per commercial account. Nobody can sustain that cognitive load across a full book of renewals. Errors slip through. When a claim later gets denied because of a missed endorsement, the brokerage faces an E&O lawsuit that can be agency-ending.

What automation looks like: structured comparison reports with human-in-the-loop sign-off. The AI reads the newly issued policy, the binder, and the expiring policy. It produces a line-by-line comparison flagging every discrepancy: coverage limits, deductibles, named insureds, endorsements, forms. Each flag points to the exact page and clause in the document. Your account manager reviews the flagged items in 10 focused minutes instead of four hours. The AI never binds anything, never emails anything, never takes autonomous action on legal documents. It does the cognitive grinding. The human makes every decision. Net effect: you catch more errors, not fewer, and the E&O exposure shrinks instead of expanding.

5. Loss run ingestion and analysis.

To remarket a commercial account, the account manager needs 3 to 5 years of loss runs from the expiring carrier. Every carrier produces them in a different format: different columns, different terminology, different claim status codes. The AM logs into the carrier portal, downloads the PDFs, and manually transcribes total claims paid, outstanding reserves, and claim frequency into a standardized spreadsheet or into a new carrier's quoting portal. One slipped decimal can completely skew the underwriter's analysis and inflate the new premium. And this happens for every single commercial renewal, on top of every other manual task the AM is already juggling.

What automation looks like: AI extraction and normalization of loss run data across carrier formats. The system ingests the PDF, extracts every claim record, standardizes the terminology, and produces a clean, carrier-neutral loss run summary. The account manager gets a ready-to-submit history with narrative context, not a stack of PDFs to retype. Quote submission time drops from half a day to an hour. Accuracy improves because the system does not transpose numbers when it reads across pages.

6. FNOL (First Notice of Loss) intake.

First Notice of Loss is the moment of truth. It is when the client actually uses the product they bought from you. And the intake workflow is fundamentally broken. A client in panic calls the agency, emails blurry phone photos of an accident, or drops off handwritten police reports. Your CSR has to manually extract 30 to 50 distinct data points to properly initiate the claim in the carrier's structured system. They have to log into the specific carrier's claims portal, re-key the loss date, location, involved parties, police report numbers, and narrative description. They then have to create a suspense to follow up with the adjuster in 48 hours. When the adjuster does not respond, the anxious insured calls your agency for a status update, and the CSR has to log back into the portal to decipher the adjuster's notes.

What automation looks like: structured intake with automatic routing. The client submits the loss through a simple form, voicemail, or email. The AI extracts the required data points from unstructured inputs (photos, narratives, documents), structures them into the carrier's required FNOL format, files the claim in the carrier's portal, and creates the suspense with a 48-hour follow-up. Your CSR does human work (de-escalating the distressed client, advising on next steps) instead of data entry. When the adjuster updates the claim, the system pulls the status and surfaces it proactively so nobody has to hunt for it.

7. Suspense and diary management.

The suspense system is supposed to be your agency's safety net. A CSR requests a loss run from a slow carrier and creates a suspense to follow up in three days. If the carrier does not respond, they extend it another three days. In a well-run agency, this is how critical tasks stay visible. In an overwhelmed agency, the daily suspense list balloons to hundreds of overdue items. The safety net stops working. Critical tasks (like binding a renewal before it expires) fall through the cracks. E&O exposure quietly accumulates.

What automation looks like: AI-surfaced urgency flags and automated follow-up sequences. The system reads every suspense, understands what each is waiting on, and triages by risk: a suspense waiting on a non-critical endorsement confirmation is not the same as a suspense waiting on a binder for a policy that expires Friday. High-risk items get surfaced to the top of the list every morning. Low-risk waiting items trigger automated follow-up emails to the external party (carrier, underwriter, client) without CSR involvement. The safety net works again, and your team spends attention on the items that actually require human judgment.

Where to start and what to expect.

Implementation is phased, not a big-bang rollout. The brokerages that succeed follow a 30/60/90 sequence with measurable outcomes at each stage.

Days 1 to 30: Map the CSR workflow end-to-end. Pick the single highest-volume bottleneck, usually carrier portal re-keying or COI issuance. Deploy the first automation directly inside your existing AMS. Measure the hours recaptured per CSR per week against a baseline captured on day one.

Days 31 to 60: Layer in policy checking and loss run ingestion for commercial renewals. Activate automated remarketing triggers on personal lines rate increases. Train one person on the exception-handling workflow. No training for the broader CSR team, because the automation runs inside the tools they already use.

Days 61 to 90: Deploy FNOL intake automation and suspense triage. Measure the impact on retention ratio, policies-per-CSR capacity, and E&O exposure. Most brokerages see the policies-per-CSR number move first. Retention moves next, as the recovered capacity turns into proactive renewal reviews.

About the "just another login" problem. We have heard this objection from every operations manager we have talked to, and they are right to have it. Your team has been burned by SaaS tools that promised seamless integration and delivered another dashboard to babysit. The automation we build does not have a dashboard your CSRs log into. It lives inside Applied Epic, AMS360, HawkSoft, your inbox, and your carrier portals. There is no new password. There is no change management burden on your front-line staff. There is just less work.

About AI hallucinations on policy checking. Your concern is exactly why we never deploy AI as a black box on legal documents. Every policy check produces a structured comparison report with flagged discrepancies pointing to the exact clause. The AI never binds. The AI never emails a client. The AI never makes an autonomous decision on coverage. It does the four hours of reading so your account manager can spend ten focused minutes on the discrepancies that actually matter. You catch more gaps, not fewer.

About implementation downtime. We do not pull your CSRs off the floor for weeks of training. The system is built and tested alongside your live operations. Training, where it is needed at all, is measured in minutes per person, not days, because we are not asking your team to learn a new platform. First measurable wins land in weeks. We work with independent insurance brokerages across Calgary and Western Canada. For pricing context across engagement scopes, see our transparent breakdown of AI costs. For the full catalogue of automation patterns we build on, see solutions.